AI Dominates, Healthcare Innovations Advance, and Financial bellwethers Set Tone on Jan 23, 2026

Today's stock market action sees AI infrastructure booming, green hydrogen scaling, key advancements in healthcare, and bellwether financial updates shaping investor outlooks.

S&P 500, Nasdaq Futures Plunge As Trump Escalates Tariff Threats | Stock Market Today

Trump says stock market will double, Goldman Sachs says gold could hit $5,400: Only one is likely

Earnings melt up in stock market will bring equities higher, says Yardeni Research's Ed Yardeni

The stock market on January 23, 2026, was largely shaped by significant developments across the technology, healthcare, and financial sectors. Artificial intelligence and cloud computing continue to drive considerable investment and strategic moves, while key advancements in medical devices and biopharmaceuticals signal potential shifts in patient care and growth trajectories. Meanwhile, regional banks report Q4 2025 earnings, and major financial institutions like JPMorgan Chase provide critical guidance influencing broader market expectations. Corporate actions, from acquisitions to debt restructuring and new market listings, also captured investor attention, painting a dynamic picture of today's economic landscape.

AI and Cloud Sector Sees Accelerated Growth and Strategic Expansion

The artificial intelligence and cloud computing space is experiencing a surge in activity, with several companies announcing strategic initiatives aimed at bolstering their positions. Plug Power (PLUG) completed the installation of 100 MW GenEco electrolyzer units at Galp’s Sines refinery. This milestone is expected to improve revenue visibility for green-hydrogen projects and could accelerate project-level cash flow recognition, according to the company. AIXC (AIXC) is actively expanding its AIxC Hub ecosystem, indicating a management focus on growth capital and partnerships to meet the escalating demand for AI infrastructure. These efforts suggest a strong commitment to capitalizing on the burgeoning AI market. Stock Titan reports further that MAAS (MAAS) announced a transaction agreement to acquire Times Good. This strategic merger aims to build a comprehensive AI ecosystem by combining computing power and algorithms, potentially accelerating product development and strengthening MAAS’s competitive standing in the AI infrastructure race. Additionally, Live Ventures (LIVE) claimed engineering an autonomous, AI-driven distribution network, reporting throughput gains of up to 10x. If validated, this operational upgrade could significantly alter logistics economics for its portfolio companies, underscoring the transformative potential of AI in operational efficiency.

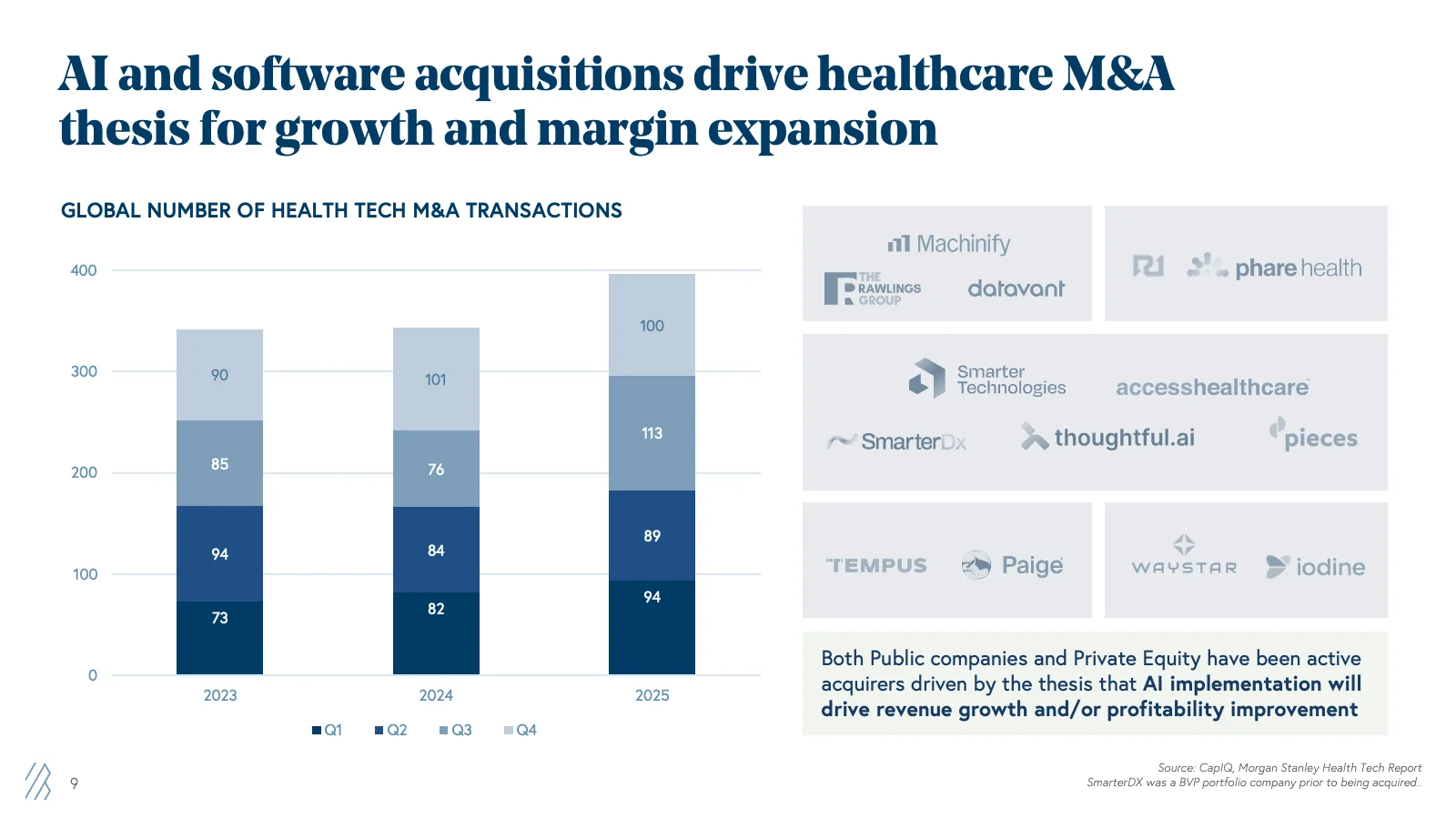

Healthcare Sector Navigates Approvals, Acquisitions, and Clinical Trials

The healthcare and biotech sectors witnessed a mix of regulatory successes, strategic acquisitions, and clinical setbacks. Medtronic (MDT) received CE Mark approval in Europe and successfully completed U.S. IDE first cases for its Sphere-360™ PFA catheter. This dual achievement could expedite the commercial rollout of atrial fibrillation therapies and support future device revenue growth. BioCryst (BCRX) completed its acquisition of Astria Therapeutics, a move that expands its presence in the hereditary angioedema market and integrates commercial-stage assets, thereby reshaping near-term growth expectations for the company. However, not all news was positive, as Ultragenyx (RARE) shares declined following its Phase III Orbit and Cosmic studies missing primary endpoints. This clinical setback raises immediate pipeline risk and is expected to impact sentiment across gene-therapy peers. Bausch Health (BHC) provided an update on its RED-C Phase 3 program, with the timing and endpoints remaining key factors for valuation and clinical risk assessment. In a testament to enduring innovation, Intuitive Surgical (ISRG) announced that its da Vinci system has now benefited 20 million patients worldwide, a durability milestone that reinforces the recurring-revenue thesis for consumables in robotic surgery, as per Stock Titan.

Regional Banks and Financial Giants Report Earnings and Strategic Roadmaps

The financial sector provided insights into profitability, credit trends, and strategic directions. Northrim BanCorp (NRIM) reported Q4 2025 EPS of $0.55 and full-year EPS of $2.87, offering a glimpse into community-bank profitability within a tightening-rate environment. Webster Financial (WBS) posted fourth-quarter 2025 EPS of $1.55 (adjusted $1.59), serving as a crucial read-through for regional-bank earnings quality and credit trends. Affinity Bancshares (AFBI) also announced its fourth-quarter 2025 financial results, contributing another data point for investors monitoring margins and loan performance in the regional banking sector. On a larger scale, JPMorgan Chase (JPM) published a company update for 2026, outlining its strategic priorities and capital plans. As a bellwether institution, JPM’s guidance on capital returns, investment-banking activity, and market-risk appetite is expected to significantly influence investor expectations across the broader financial industry.

Corporate Maneuvers: Acquisitions, Debt Reduction, and Market Listings

Several companies announced significant corporate actions impacting their capital structure and market presence. Equinox Gold (EQX) successfully closed the sale of its Brazil operations for US$1.015 billion. The company utilized these proceeds to pay down more than US$800 million of debt, reducing its net debt to approximately US$150 million and materially lowering its leverage. FedEx (FDX) launched senior notes tied to its Freight spin-off, with the debt financing for this carve-out deemed pivotal for pro forma leverage and the timing of the separation. In terms of market access, EquipmentShare (EQPT) debuted on Nasdaq as EQPT, signaling investor appetite for construction-tech companies that digitize heavy-equipment fleets. Moomoo (FUTU) expanded retail access to the BitGo IPO with broad subscriber participation, a development indicating that platforms are widening retail IPO channels, which could boost demand dynamics for in-demand listings, as highlighted by Stock Titan. Lastly, Janus Henderson (JHG) announced the acquisition of Richard Bernstein Advisors, a strategic buy intended to strengthen its active-management capabilities and potentially expand its distribution network.

Operational Readiness and Small-Cap Liquidity Concerns

Utilities demonstrated proactive measures in response to anticipated weather challenges, while small-cap companies faced liquidity and compliance issues. CenterPoint Energy (CNP) activated staging sites and increased emergency-response capacity ahead of a winter storm, aiming to reduce outage risk and inform near-term operating contingencies. Similarly, FirstEnergy (FE) confirmed its crews were ready for an approaching winter storm and offered safety tips to customers, underscoring how utilities’ operational readiness can curb outage durations and protect near-term reliability metrics. Meanwhile, NeoVolta (NEOV) announced a $10 million equity offering, and Daxor (DXR) filed a $9 million registered direct, both moves designed to extend their operational runways but also potentially diluting existing shareholders. Revelation Biosciences (REVB) announced the exercise of warrants for approximately $11 million in gross proceeds, providing a near-term liquidity boost for the small biotech. Multiple small-cap issuers also received Nasdaq notices or provided governance updates, with Digital Currency X (DCX) receiving a delisting notification, and XTL (XTLB), K Wave Media (KWM), and BMGL reporting equity/compliance deficiencies—issues critical for their liquidity and potential restructuring.

Related Articles

Joby Aviation Stock Tumbles 13% on $1 Billion Capital Raise Plan

Joby Aviation shares dropped significantly after announcing plans to raise $1 billion through stock and convertible note sales, sparking dilution fears among investors.