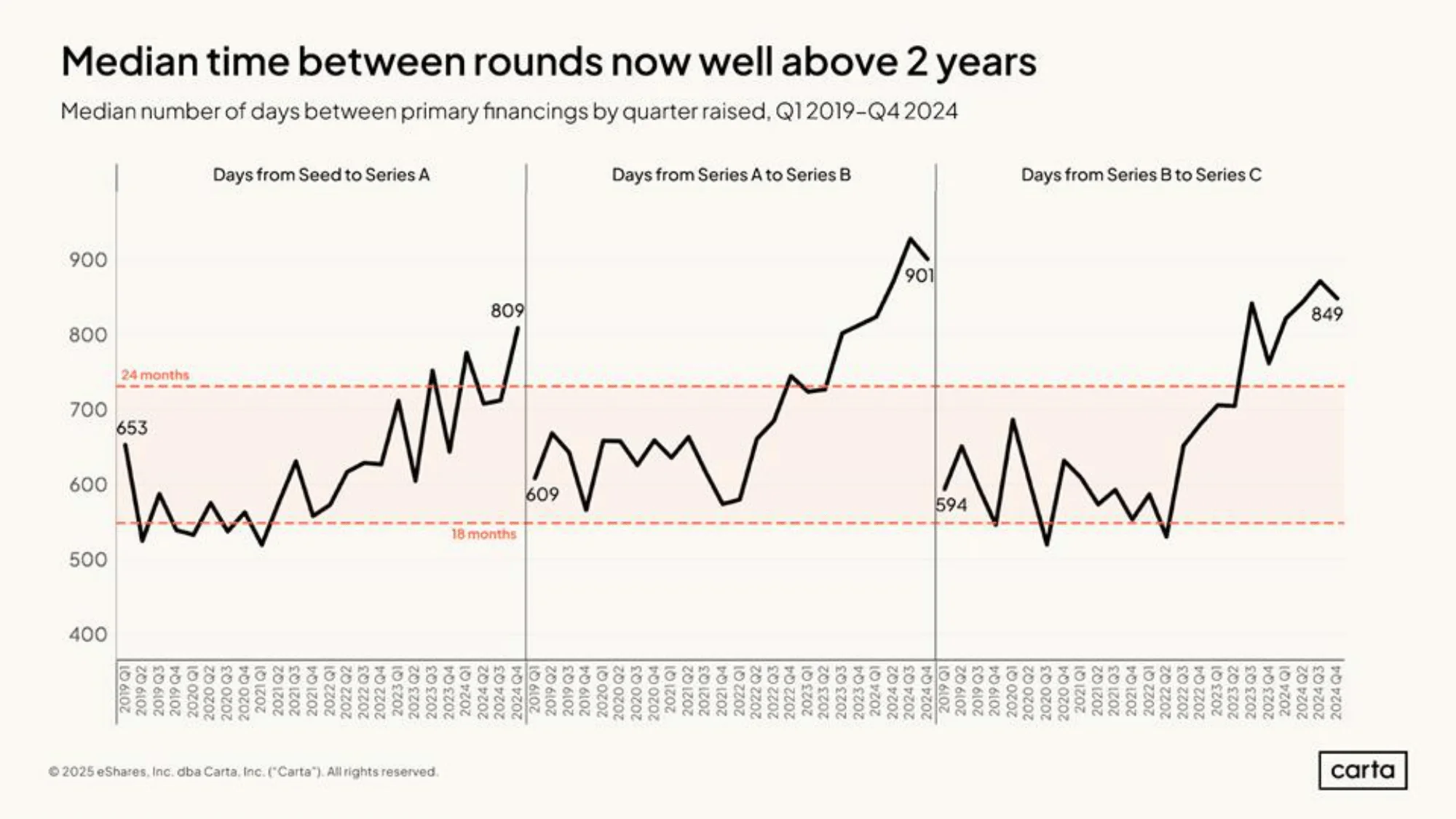

Only two US states, California and Washington, saw their share of venture funding rise last year, driven by a 46% surge in North American startup funding, primarily in AI. Deep tech ecosystems are vital for future growth.

In a year that saw a significant 46% surge in North American venture investment, primarily fueled by the burgeoning artificial intelligence sector, a stark geographical concentration of capital has emerged. Only two states with established venture ecosystems, California and Washington, managed to increase their share of total U.S. startup funding in 2025. This consolidation, as highlighted by a recent CryptoRank report, underscores a critical trend: while overall investment is up, the rising tide isn't lifting all boats equally. California, the perennial powerhouse, absorbed a staggering 64% of nationwide investment, signaling an ever-tightening grip on the venture landscape. This phenomenon raises important questions about the nature of innovation hubs, the future of work in an AI-dominated world, and the pathways for other regions to cultivate competitive deep tech ecosystems.

The concentration of venture capital is not a new phenomenon in the United States, but the intensity and drivers of the recent surge offer a fresh perspective. Historically, innovation has clustered around established centers like Silicon Valley due to a confluence of factors: access to top-tier universities, a deep talent pool, a supportive regulatory environment, and a robust network of venture capitalists and angel investors. The 2025 data, as analyzed by CryptoRank, indicates that this clustering effect is accelerating, particularly in the wake of the AI boom. While states like New York, Massachusetts, and Texas also saw significant investment bumps, their share relative to the national pie either held steady or declined slightly, despite substantial absolute dollar increases. This suggests that the sheer volume of AI-driven capital directed towards California and, to a lesser extent, Washington, is disproportionately reshaping the investment map. The "deep tech" nature of many AI innovations, requiring extensive research and development, often benefits from established university-industry pipelines and specialized talent found in these key hubs.

The 2025 venture funding landscape painted a clear picture of concentration, with AI acting as the primary catalyst. North American startup funding soared by an impressive 46% year-over-year, yet only California and Washington managed to increase their proportion of this expanded pie. California maintained its dominant position, capturing an overwhelming 64% of all U.S. venture funding. This signifies not just growth, but a deepening of its lead over other formidable venture ecosystems. For instance, while New York, Massachusetts, and Texas are robust funding hubs, they saw their relative shares either remain constant or slightly diminish, despite attracting significant absolute capital. New York's major rounds included predictions marketplaces Polymarket and Kalshi, and AI coding startup Reflection AI. Massachusetts, known for deep-tech, saw fusion energy pioneer Commonwealth Fusion and brain-computer interface developer BrainCo lead its funding. Texas, particularly Austin, drew investment for residential backup battery provider Base Power and autonomous maritime vessel developer Saronic. Washington’s diversified scene saw major rounds for nuclear power company TerraPower and reusable rocket developer Stoke Space. Even states like Colorado saw substantial investments, with AI infrastructure company Crusoe raising $1.4 billion and quantum computing startup Quantinuum securing $600 million, yet these didn't significantly alter the overall national distribution trend. Florida, Pennsylvania, Illinois, North Carolina, and Virginia each pulled in over $2 billion, and another seven states – Utah, Tennessee, Maryland, Ohio, Minnesota, Georgia, and New Jersey – attracted over $1 billion. However, collectively, these 12 states captured only about 11% of all nationwide investment, underscoring the extreme concentration at the top, as detailed by CryptoRank. This trend aligns with discussions around the need for robust deep tech ecosystems to attract such capital, as articulated by Kris Gopalakrishnan, co-founder of Infosys. Speaking at the India AI Impact Summit, Gopalakrishnan emphasized the necessity for countries like India to translate academic research into tangible products to build a strong deep tech environment, which in turn attracts global investment. This sentiment resonates with the investment patterns observed in the U.S., where states with strong research institutions and an ecosystem that fosters product development from laboratory work tend to thrive in attracting deep tech funding, as reported by The Economic Times.

The intense concentration of venture funding in California and Washington, predominantly driven by AI, highlights a critical and evolving dynamic in the global technology landscape. This isn't merely about capital flow; it's about the fundamental characteristics of innovation in the age of deep tech. Deep tech ventures, by their very nature, require extensive R&D, specialized scientific talent, and long-term investment horizons. They often emerge from academic research and thrive in environments where there's a strong nexus between universities, industry, and government funding. The success of California and Washington in capturing an outsized share of this investment suggests they possess these foundational elements in abundance, allowing them to translate bleeding-edge research into productization at scale.

However, this trend also casts a long shadow over the broader tech sector, particularly established legacy firms. Venture capitalist Vinod Khosla's provocative assertion that 15-20 year veterans at companies like Cisco are 'unemployable' due to rapid AI advancements, as reported by Whalesbook, underscores a significant talent disruption. Khosla argues that the agility and continuous learning characteristic of startups, particularly in emerging technologies, now command greater trust than the experience accumulated within established giants. This perspective suggests an accelerated obsolescence of traditional IT expertise, forcing established players like Cisco, IBM, and General Electric to fundamentally retool their workforce and strategies or face increasing irrelevance. The market capitalization and P/E ratios of these legacy firms, while still substantial, may not fully price in the systemic threat posed by AI to traditional business models and the erosion of their core talent advantage. The implication is clear: the future of technological leadership is shifting from those who maintain legacy systems to those who rapidly innovate and adapt to deep tech paradigms.

The success of the leading states and the challenges faced by others underscore the critical importance of a robust ecosystem that goes beyond just funding. As Kris Gopalakrishnan rightly stated, "We have to translate our research into products and technology. We don't have that kind of ecosystem and culture yet" in many developing economies, including India, which he discussed at the India AI Impact Summit, according to The Economic Times. This sentiment applies equally to many U.S. states struggling to compete with the likes of California and Washington. The creation of such an environment, rooted in academic and laboratory research, is essential not only for domestic innovation but also for attracting international capital. Gopalakrishnan highlighted successful models like the research park at IIT Madras, where industry research is co-located with academic research, fostering direct collaboration. Similar initiatives at IIT Bombay and IIT Delhi are proving effective in bridging the gap between theoretical knowledge and practical application. Furthermore, industry-led programs, such as the Confederation of Indian Industry's initiative to connect enterprises with startups to solve shared problem statements, offer a blueprint for fostering innovation and channeling investment beyond traditional venture models. These strategies are vital for states that aim to increase their share of deep tech and AI-driven venture funding, rather than merely benefiting from general economic upturns. The focus needs to shift from simply having strong universities to actively creating mechanisms that propel research out of labs and into the marketplace, forging talent pathways for the next generation of deep tech innovators.

The trends observed in 2025 suggest that the geographic concentration of venture capital, particularly in AI and deep tech, will likely intensify in the short to medium term. For states seeking to increase their share of national funding, the blueprint is clear: investment in foundational research institutions, fostering robust industry-academia collaboration, and cultivating an environment that champions the translation of cutting-edge science into marketable products. This requires a long-term strategic vision, moving beyond merely attracting tech companies to building self-sustaining innovation ecosystems. Furthermore, the implications for the global talent landscape are profound. As Vinod Khosla's stark comments highlight, continuous learning and adaptability in emerging technologies will become paramount, challenging traditional career paths and demanding a re-evaluation of workforce development strategies. The future success of nations and regions will increasingly hinge on their ability to cultivate and retain talent capable of navigating and driving this technological transformation, ensuring that the promise of AI lifts more than just a select few boats in the ever-evolving venture capital sea.

Google and Accel's Atoms accelerator rejected 70% of AI startups as 'wrappers,' highlighting a venture capital pivot towards deep tech and proprietary models over superficial integrations.

Qualcomm Ventures launches a $150M Strategic AI Venture Fund to back Indian AI startups in automotive, robotics, IoT, and mobile sectors, coinciding with India's projected AI market surge to $32B by 2031.

San Francisco-based tech startup Temporal, a leader in distributed systems reliability for AI applications, has secured a massive $300 million Series D funding round led by Andreessen Horowitz, doubling its valuation to $5 billion amidst surging demand for robust AI infrastructure.